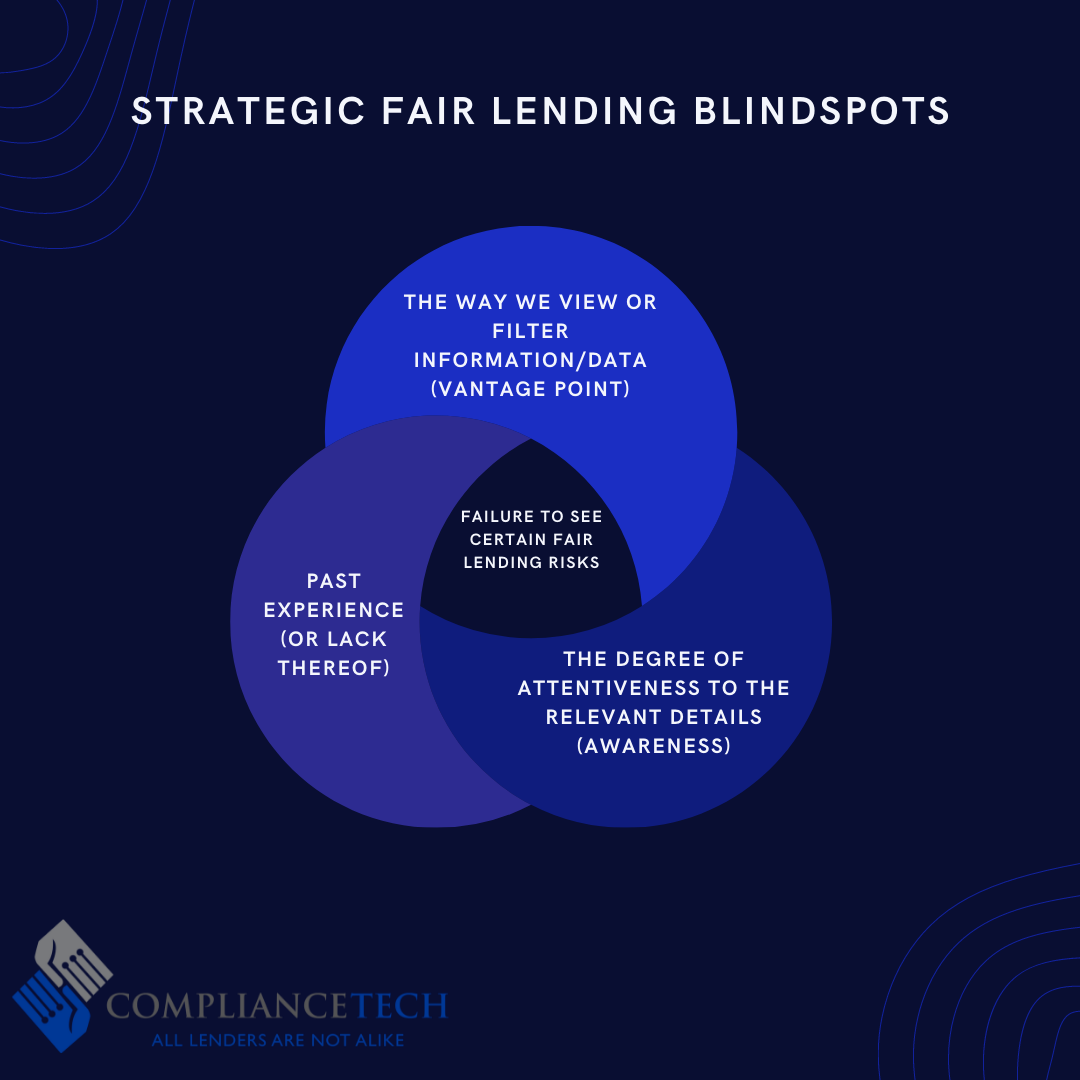

Normally, when one thinks of the term “blind spot” our mind immediately goes to driving a car and what we can’t see in either our rear-view or side-view mirrors. What we cannot see is affected by our past driving experience, our vantage point or our location in the seat, the size/type of mirrors (tools to detect), and our attentiveness. Extending the automobile blind spot metaphor to the subject at hand, a strategic fair lending blind spot is defined as the failure to see certain fair lending risks usually due to the following: (1) past experience (or lack thereof); (2) the way we view or filter information/data (vantage point), or (3) the degree of attentiveness to the relevant details (awareness). In most cases, a blind spot will be something you can’t see which may be obvious or in plain view of others.

The reason blind spots happen is that something is obstructing our view of reality. In the automobile situation, the obstruction is usually something physical. In a business decision-making context, the obstructions are often psychological or analytical. When we unbundle the psychological we find the concepts of biased/unchallenged assumptions, confirmation bias, hindsight bias, and information deficit or filtering. With biased/unchallenged assumptions we have an idea in our head that we cannot shake despite data to the contrary. In groupthink situations, this becomes the prevailing view when those assumptions go unchallenged. In the case of confirmation bias, the decision-maker looks only for evidence to support their biased assumption while ignoring strong evidence to the contrary. Hindsight bias is similar in that past factual events are distorted or misinterpreted to justify a misguided course of action. Finally, an information deficit involves not possessing the requisite information to make a sound decision; and information filtering is selectively accepting facts from the data to support a biased assumption. These causes of blind spots concepts are not mutually exclusive of each other and frequently occur in combination.

As with the driving analogy, fair lending risk managers experience blind spots on a regular basis with few negative consequences. The negative consequences occur when the lender is sued by the government or private litigant. Such lawsuits should not be a surprise but this is usually not the case if the lender is operating with blind spots. This article explores ten common issues that can blind lenders of fair lending risks.

1. Lack of awareness of what constitutes “fair lending.”

More likely than not, a lender can be blinded by a faulty notion of what constitutes “fair lending”. If a lender believes that fair lending is largely about not being racist or prejudice then the lender may be blinded to fair lending risks resulting from unintentional discrimination. Discriminatory intent or racial animus is not a required element to prove a violation of the Equal Credit Opportunity Act (ECOA) or the Fair Housing Act (FH Act). One only needs to review the cases brought by the U.S, Department of Justice over the past 20 years to see that the vast majority do not involve overt discrimination with evidence of discriminatory intent. Most of the cases involve disparate treatment resulting from statistically significant differences in outcomes for one group versus another. Bottom line: develop a broad view of fair lending that encompasses all strategic lending and servicing decisions.

2. Failure to prepare quality HMDA data.

Using the car analogy, the HMDA data are like mirrors to help you see an approaching risk that might be discovered during a fair lending exam. As is typical with most blind spots, these are risks that the inattentive lender does not see while such risks are really visible to others. There is hidden risk in looking at overall approval/ denial disparities without paying attention to other HMDA action categories for applications that were neither approved nor denied. But nevertheless fell out of the pipeline. A thorough analysis of all action categories may reveal a need to redefine what constitutes an “application: for HMDA reporting purposes. This issue alone can have a dramatic impact on the statistical analysis of lending disparities. Another HMDA data quality issue includes the underreporting of race and ethnicity information. This tends to happen more when the application is taken via the telephone or internet. The HMDA rules allow the lender an out in these cases. Over the years we have found that the medium of data collection matters less than how the lender consistently requests the government monitoring information from its applicants.

Bottom line: Institute internal controls to ensure HMDA data accuracy. Make sure you benchmark your performance rates to your industry peers. Standardize and enforce protocols for collecting government monitoring information especially if you have a significant percentage of telephone, Internet, and broker applications. If possible, tie HMDA accuracy to originator compensation.

3. Failure by the lender to see the relationship between the demographics of the market and the expected level of applications from minority groups.

While this may seem like an obvious blind spot to address it continues to appear in the HMDA data. It is not uncommon to see a lender obtain 1000 or more white applications in say the Baltimore or Atlanta market while failing to receive an expected level of applications from African-Americans commensurate with their population percentages. The same is true in markets dominated by Hispanic populations. It is true that African Americans and Hispanics have a lower homeownership rate and therefore lower demand for credit may be expected. This can explain some of the discrepancies but usually not all of them. Bottom line: Evaluate the racial demographics of every market where you have significant levels of white applicants and then set reasonable target levels for applications from dominant minority groups. Next, assemble the human resources to meet those targets.

4. Failure to see the connection between the complexion of your origination resources and your HMDA origination outcomes.

This is the lack of diversity blind spot. It never ceases to amaze me that seemingly well-intended lenders who want to succeed at fair lending fail to see that the diversity of the origination team has a direct impact on fair lending risks. The mortgage origination business, especially for home purchase financing, is a relationship-based referral business. Real estate professionals come in all shapes, sizes, and colors. Originators who can connect with real estate professionals in a variety of wars (family, community, church, schools) are likely to be more successful because it is in their economic self-intent to help each other. A unique diversity blind spot appears of the lender relies on 3rd party brokers because of the paucity of minority brokers in every market. This represents a tremendous strategic opportunity for a creative lender who can figure out a way to grow and develop a group of minority brokers in key markets. Bottom line: Racial diversity of the mortgage origination team is an antidote for problematic lending patterns.

5. Marketing blind spots.

The Fair Housing Act is clear that marketing related to housing and housing finance should be free from bias. Over the years HUD has mostly challenged the real estate sales community on the Ads that portray only whites. While there have not been a ton of lending cases on Ads, lenders can be vulnerable. The problem rarely occurs these days with the largest lenders that have established culturally sensitive marketing teams. The problem is seen most often with mid to small-sized mortgage companies and banks. Therefore, consciously make sure your print Ads have people in them that look like the communities to which you are marketing. Another less obvious marketing blind spot involves the rental of mailing lists for refi or home improvement loan marketing. Be careful not to seek lists based on narrow criteria like average loan size, expected equity, and estimated home value. While none of these criteria are illegal, excess reliance on them is certain to skew your HMDA data towards white neighborhoods. Bottom line: Ask yourself about the possible fair lending impact of all marketing decisions.

6. Assumption: that race and ethnicity are the only issues to worry about.

Because of the required HMDA reporting of race and ethnicity, there is a tendency by lenders to only worry about risk monitoring for these prohibited bases and call it a day. This could lead to serious fair lending risk blind spots for gender, age, marital status, disability, receipt of public assistance, and several other prohibited bases identified in ECOA and the FH Act. Gender is reported under HMDA. Age is easily determined from the date of birth on the loan application. Both gender and age lend themselves to the same type of rigorous statistical analysis as you would do for race and ethnicity. That is not the case for all of the other prohibited bases. For these, you will want to get members of compliance, marketing, credit policy, underwriting, production and servicing together to make assessments of your risk exposure with regard to these other protected groups.

7. Assumption: black and Hispanic applicants of low/moderate income are causing my denial disparity.

This assumption is usually wrong although I am not sure why it is the case. Operating under this assumption will make the lender more vulnerable to fair lending risk when income is being controlled for. It can also affect the design of marketing efforts to low/moderate-income applicants. Suffice it to say, you are more likely to encounter difficult to explain disparities and match pairs among the higher income applicants than the low/moderate income group although our intuitions suggest otherwise.

8. Failure to elevate fair lending as a major risk area and organize a team structure to get fair lending done.

This situation evolves from an assumption that it is not such a big deal that I need to dedicate significant resources toward it. Examples of this are making the person responsible for compiling and reporting HMDA the person responsible for managing fair lending risk. It is hard to do both and fair lending monitoring requires a higher skill set than HMDA reporting. In addition, the fair lending person should be of sufficient rank and status to be able to influence policies in marketing, credit underwriting, product development, and originator recruitment. To prevent fair lending risk blind spots the fair lending representative needs to have an equal seat at the table.

9. Failure to integrate the customer complaint process with fair lending monitoring.

Customer complaints can be a wide-open door to fair lending risk. Here is a case in point. Few people know that the automobile fair lending pricing cases we are hearing more about today began in the late ’90s as a lemon law complaint directed at the dealer. Ms. Cason, an African-American woman, to her case to a solo practitioner who noticed how much she was being charged who turned to industry experts to pursue the ECOA angle of lender participation in finance charge markups over the buy rate at which the applicant was qualified for. This would be called an overage in mortgage industry parlance. This little case blossomed into numerous class actions against auto finance companies in the past. The CFPB is continuing to investigate these types of issues today.

Bottom line: Make sure you are maintaining a complaint database system that allows you to pay attention to any complaint that could become a fair lending issue down the line.

10. Viewing your HMDA data out of context and through rose-colored glasses.

This is an example of filtering information to reach a desired outcome. No analysis of HMDA lending performance is valid if it does not compare the subject lender’s performance to industry benchmarks, market average, and peer competitor. There are inexpensive automated tools available that make in-context HMDA analysis easy to perform.

Bottom line: An isolated lender-only analysis means very little without peer comparisons.

Conclusion: 360 View of Fair Lending Risk

The purpose of this article is to provide a framework for understanding hidden risks in fair lending. We defined fair lending risk blind spots and how they can arise through biased/unchallenged assumptions, confirmation bias, hindsight bias, and information deficit or filtering. We listed 10 areas of fair lending risk where blind spots can occur and offered guidance on how to unhide these risks. Our final recommendation to lenders is to develop an integrated team approach to fair lending that comprehensively observes fair lending risk management from different perspectives. Such an integrated approach would combine concepts of diversity, marketing, goal-setting, channel strategy, peer analysis, real estate professional relationship building, and community outreach. The challenge may sometimes appear daunting and even puzzling. However, minimizing fair lending risk blind spots is achievable if you are intentional about what you want to accomplish and you work as a team.

This article was originally written by Debby Lindsey and Michael Taliefero for the Mortgage Compliance Magazine. Please don’t hesitate to reach out to us online.