In my experience, there are more lenders who do little to nothing to monitor fair lending than those who actively manage it. Those that do less tend to be independent mortgage companies rather than depository institutions.

I believe there are several reasons for this outcome:

A) Culture and Traditions: Prior to Dodd-Frank independent mortgage companies were not subject to compliance examinations. Therefore, many of them just do not know what it takes to get ready for a fair lending examination. In many cases, the sales culture of such lenders dominate the risk management side of the business.

B) The only color they see is green. Because of the entrepreneurial nature of mortgage companies, they would like to think that the desire to make every loan effectively prevents lending discrimination.

C) The absence of a Community Reinvestment Act (CRA) imperative directed to lending to low and moderate-income households and in LMI areas. The monitoring and reporting disciplines and institutional framework required by CRA create a more receptive climate for fair lending monitoring.

D) Some mistakenly believe “the darned if I do or don’t rhetoric.” This says, for example, if I increase credit access it will cause more fair lending problems.

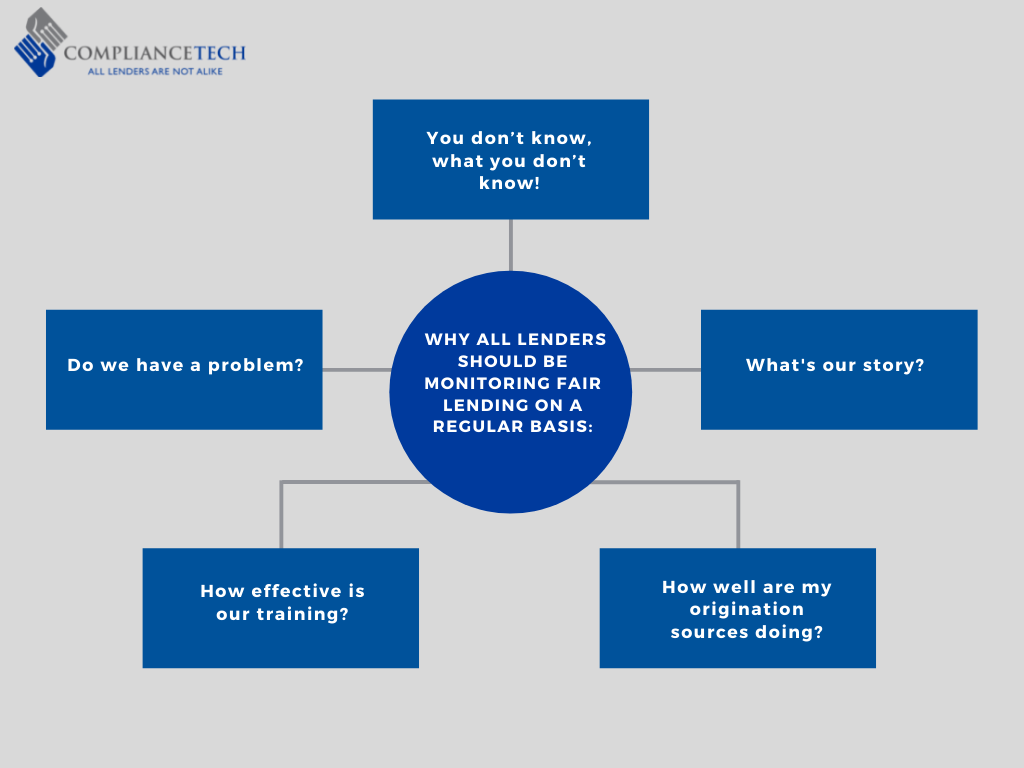

Notwithstanding these possible reasons for doing less fair lending monitoring, I would like to offer the following 5 reasons why all lenders should be monitoring fair lending on a regular basis:

- You don’t know, what you don’t know! Fair lending monitoring will inform the lender about operational gaps and missed opportunities never considered.

- What’s our story? Every lender has a different narrative based on its chosen business model. It is important to be able to explain your lending performance to a regulator in that context as well as relative to peers. How does the lender look from the outside?

- How well are my origination sources doing? When you monitor fair lending activity by channel, loan officer, or broker the lender can then see patterns that may be hidden when all activity is averaged in the aggregate. A related issue is whether marketing activities support or detract from fair lending?

- How effective is our training? Fair lending monitoring gives rise to findings which sometimes requires re-training staff in certain areas. Regular monitoring allows the lender to measure the effectiveness of the training and hold employees accountable.

- Do we have a problem? Lenders generally consider this to be the most important reason to act. Unfortunately, this is not a question to be asked just once: It must be asked over and over; every quarter, every year, in multiple markets for each channel and for various products.

If you have been sitting on the fair lending sidelines, hopefully, this note will inspire you to act. Like quality assurance, fair lending monitoring is an essential business practice. Believe it or not, once you get into it, you will find it intriguing. Feel free to send any questions or comments to www.Compliancetech.com.